Lihaa luiden ympärille!

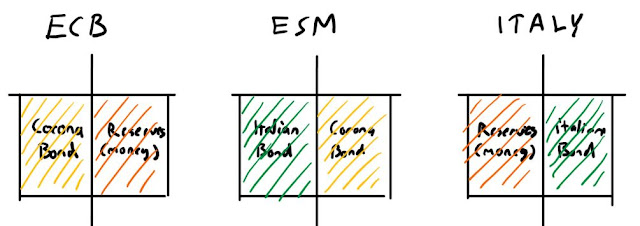

Lihaa luiden ympärille! Seurattuani pari päivää Jussi Ahokkaan ja Juhana Siljanderin mielenkiintoista keskustelua twitterissä, innostuin piirtämään hommaa omasta perspektiivistäni auki. Liittyy mm. seuraavaan twitter-ketjuun: https://twitter.com/ahokasjaj/status/1265587056966844417 Punaisella loppusaldojen muutokset. T=0. Lähtötilanne, meillä on keskuspankki, pankki A, valtio ja yritys. Taseiden summa 200$. T= 1. Valtio liikkeellelaskee 100$ velkaa, yksityinen sektori lainottaa (pankki A ja yritys). Valtio saa 100$ pankkitalletuksia tililleen pankissa A. Taseiden summa 350$. T=2. Valtio kuluttaa 100$ yritykseltä tilattuun rakennusprojektiin. G: +100$ Taseiden summa 450$. T=3. Keskuspankki aloittaa QE-ohjelman ja ostaa valtionvelkakirjat pankilta ja yritykseltä. Pankki saa 100$ reservejä ja yritys 50$ lisää talletuksia. Huomataan, että pankilta ostettaessa, kyseessä oli vain "asset swappi", mutta yritykseltä ostettaessa pankkitalletusten ...